Well, here we go folks. They've done it again. The Alibaba Accounting Department, after a couple of fits and starts and a month delay, at the 11th hour, finally managed to file yet another, laugh-out-loud, gut-buster of a 20-F Annual Report. Needless to say, as always, they did not disappoint!

Financial Comedy Genius!....Kudos!.....Bravo! Like a George Lucas franchise, just when you thought it couldn't possibly get any better, they come up with the financial equivalent of "Jar Jar Binks".

It's a page turner...it has to be....it's 233 pages with an additional 93 pages of circular footnotes, charts and tables, laden with nonsensical, legal sounding gibberish that would make a Securities Lawyer blush with envy and/or question his virility. I've spent the last few evenings going through it (I have a day job...) and I have to say, I couldn't put it down. It's riveting.

Sadly, in this issue, they've left out the family photos, advertising and screen shots of the fake/knock-off products they sell, presumably to save some space. My guess is that some dull-as-a-butter-knife PWC accountant probably talked them out of including the personal, Horatio Alger scrap-book stuff. It's a shame really.

So let's start with the press release......it sets the tone:

The company aims to build the future infrastructure of commerce. It envisions that its customers will meet, work and live at Alibaba, and that it will be a company that lasts at least 102 years.

https://www.businesswire.com/news/home/20180727005591/en/

Yup....that's right....they are guaranteeing that the company will be around not 100 years, not 101 years.....but at least 102 Years! Alibaba will be my (our) life....Alibaba is where we will live, work, meet and eventually be buried.....we'll raise our kids there and our pets will poop on our little slice of heaven that is the Alibaba front lawn. Kind of creepy if you ask me.

As an aside...why aren't they issuing 102 year bonds to show their confidence in the business model?

As always, for your convenience, and because I value your time, feel free to read the RED Executive Summary at the beginning of each section. If the topics don't pique your curiosity, you can move along to the next section and the next Executive Summary as the spirit moves you.

The Capital Structure...(Now you see it....now you don't...)

Executive Summary: In this section we explore the following observations:

1.) There are now 920 separate operating entities in the Alibaba ecosystem. 500 in the PRC and 420 scattered all over the rest of the planet. Alibaba has created 300 new "legal" entities a year for the last two years.

2.) They've "Enhanced" their Capital Structure. The lawyers have been busy beavers.

3.) Major Business Segments and Operating Entities appear and disappear from the 20-F's. There is no explanation in the footnotes.

So where do we start? As you my readers know, I like to jump into really, really important, seemingly innocuous documents (Like Chinese 20-F's) which most people, without a ton of effort, generally can't begin to understand. By virtue of this lack of understanding, they (understandably) don't seem to care too much about these documents until there's a painful enlightenment smacking them in the face somewhere down the road....followed by a chorus of "if only I'd understood this!" and the consequent, requisite Congressional hearings focusing on "blame delegation". That's where I try to add value. I try to help good folks like you, my cherished readers, see what's just over the horizon. As always, I'm here to help.

So, speaking of "things we can't begin to understand without putting in a ton of effort" let's start out by talking about Alibaba's Capital Structure......I know, I know.....stop jumping up and down with glee....try to contain yourselves. It's just accounting.....Geez....

So like we always do with an Alibaba 20-F review, with absolutely no rhyme nor reason, let's pick a random page.....let's start on page.....Oh....I don't know.....how about page 115?

It starts off with some some wonderfully amazing information:

As of March 31, 2018, we conducted our business operations across approximately 500 subsidiaries and consolidated entities incorporated in China and approximately 420 subsidiaries and consolidated entities incorporated in other jurisdictions.

That's right, Alibaba now has 920 Separate Operating Entities! Over the last two years Alibaba has created, out of thin air, or acquired, roughly 300 material Operating Companies per year. That's roughly 600 new businesses, one new company every business day for two years. The Alibaba lawyers have been working a ton of overtime. They must be exhausted.

Let's pause for a moment of silence.....in solemn gratitude.....for the lawyers.

Moving along, Exhibit 8.1 (Ref: on Pg 231) lists "Significant Subsidiaries & Consolidated Entities". There are forty-six (46) businesses apparently deemed to be significant. Sixteen (16) of these businesses are located in the PRC (China), Twelve (12) in the Caymans, Nine (9) in the BVI, Six (6) in Hong Kong, Two (2) in Singapore and finally, One (1) in Luxembourg.

https://www.sec.gov/Archives/edgar/data/1577552/000104746918005257/a2235254zex-8_1.htm

So, I guess, by definition, the remaining 874 businesses (920 - 46) are "insignificant"?

When we drill down a little farther we see that there are really only fifteen (15) businesses that I'll call "Super Significant" (See the Chart on Pg. 115 below)

And of these fifteen (15) "Super Significant" businesses, three (3) of them are brand spanking new in the last fiscal year! And what's really weird, is that Zhejiang Cainiao Supply Chain Co., Ltd., Youku Internet Technology and Youku Information Technology aren't even on the list of "Significant Subsidiaries & Consolidated Entities". (Exhibit 8.1) Is it a typo? So maybe they are not Significant? Just "Super Significant". Puzzling to say the least....

Zhejiang Cainiao Supply Chain Co., Ltd. is only mentioned once in the report, on page 91 under "Regulation of Foreign Investment"

The only time Youku Internet Technology is mentioned in the report is on pg 119 as a party to a contract that "Gives us Control over VIE's". Youku Information Technology is not mentioned at all....here's the ridiculous language re: Youku Internet Technology....

The parties to the loan agreement for each of our material variable interest entities are Jack Ma and Simon Xie or other shareholders of those entities (in respect of the existing VIE structure) or, following the VIE Structure Enhancement, the relevant PRC investment holding company, on the one hand, and Taobao (China) Software Co., Ltd., Zhejiang Tmall Technology Co., Ltd., Alibaba (China) Technology Co., Ltd., Zhejiang Alibaba Cloud Computing Ltd. and Youku Internet Technology (Beijing) Co., Ltd., the respective wholly-foreign owned enterprise, on the other hand.

Forget for a moment that there are now oodles of undisclosed/un-described loan agreements all over the planet with insiders, which is frightening enough, now, on one hand (or the other) we have three new "Significant" businesses, we know nothing about, that have somehow just shown up in the filings this year, that are somehow being "Enhanced".

Let's dig a little further.

When we look at last years (20-F YE 3/31/17 pg. 111) chart we see that Alibaba.com Limited (Caymans) and Alibaba.com Investment Holding Limited (BVI) are both missing from this year's chart, yet they are still included on Exhibit 8.1. A text search of the pdf shows that, oddly enough, the only other time they are mentioned in the filing is in the biography of Walter Kwauk. So where did these "Significant" businesses go? Are they still relevant?

Walter Teh Ming KWAUK ( ) has been our director since September 2014. He previously served as an independent non-executive director and chairman of the audit committee of Alibaba.com Limited, one of our subsidiaries......

) has been our director since September 2014. He previously served as an independent non-executive director and chairman of the audit committee of Alibaba.com Limited, one of our subsidiaries......

Since Mr. Kwauk is on the Alibaba Board, and is, in fact, the head of the Alibaba (BABA) audit committee and amazingly "satisfies the criteria of an audit committee financial expert as set forth under the applicable rules of the SEC" (Pg. 184) perhaps, with all of this expertise, he can tell us why the hell these two businesses were removed from the Alibaba Org chart? ....or maybe help us figure out what the three brand-spanking-new businesses that just showed up actually are?

VIE Structure "Enhancement"

Everyone pretty much understands the structure of the Alibaba ecosystem. In broad brush, general terms, it's a group of 36 "partners" listed on page 176 of the filing, who are charged with the responsibility of scouring the world for cash.

Through a convoluted web of dubious financial entities (now 920 in number), designed to meet the legal requirements of Chinese "ownership" and un-auditability, the partners, after careful deliberation, vote to piss away the money raised on kickbacks and political payoffs, in exactly the direction Jack and the CCP tell them to piss it, adjusting for wind, as needed.

Now, you'd think that this would be a pretty easy (and fun) set of marching orders to follow, but over time, we all know how confusing, off-track and complex financial shenanigans can get. Fortunately, last year, Alibaba's lawyers finally grabbed the bull by the horns and undertook a massive effort to simplify Alibaba's capital structure. So let's see what they did, keeping in mind that there are 920 entities in the BABA ecosystem now, with 420 "offshore", mostly located (presumably) in Hong Kong, the Caymans and BVI.

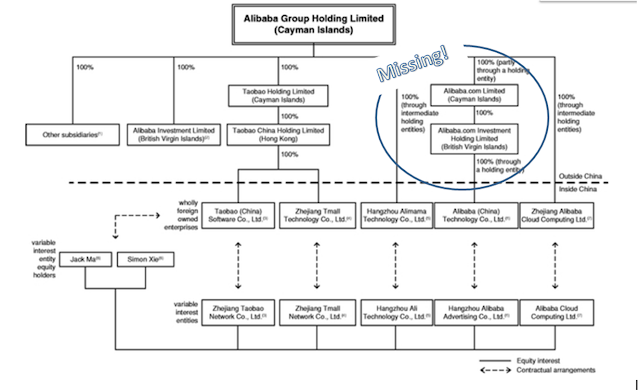

On pg. 116 of the filing, management describes the "VIE Structure Enhancement". This is the summary (in actual English "words") of what they were doing....followed by a "simple" diagram.

Upon the completion of the VIE Structure Enhancement for each VIE, the equity interest of each such variable interest entity will, instead of being held by a few individuals, be directly held by a PRC limited liability company, which in turn will be indirectly held (through a layer of PRC limited partnerships) by selected members of the Alibaba Partnership or our management who are PRC citizens. This new structure institutionalizes the governance framework of our VIEs.

Isn't that Awesome (and really smart sounding)! The diagram below describes how the legal structure of the Variable Interest Entities looked BEFORE the "Enhancements" got underway.

Pretty simple huh?

1.) BABA owns WFOE's through offshore shells (Cayamans/BVI/HK)

After the "Enhancement"....

1.) BABA owns WFOE's through offshore shells (Cayamans/BVI/HK).

2.) The WFOE's enter into contracts and agreements with the VIE's.

3.) Each VIE is owned by a PRC Investment Holding Company.

4.) The PRC Investment Holding Company is owned by various Limited Partnerships.

5.) The Limited Partnerships are owned by Individual Limited Partners and various PRC LLCs as General Partners.

6.) The General Partner LLC is owned by individual shareholders and/or PIE's (Political Insider Elite's).

7.) The WFOE's negotiate contracts and agreements in exchange for loans/cash with ALL of the above entity types.

8.) Again, there are now 920 entities involved in the Alibaba ecosystem and I'd suspect that the number will be growing geometrically.

The consolidation of all of these entities, VIE's and WFOE's - "Wholly-Foreign Owned Enterprises" is described in F-18 (Footnote 2(c)) Feel free read through the painful details of this footnote if you have the stomach. The only thing that pops out is that these entities, combined are a relatively small piece of the pie. Total Liabilities are RMB 61.699 Billion compared to Total Assets of RMB 54.463 Billion (i.e. insolvent by RMB 7.236 Billion) Compared to BABA's Total Balance sheet of RMB 717 Billion.

I, for one, am so glad that Alibaba management has finally acknowledged, through this new Capital Structure "Enhancement", their obligation to be forthright and transparent in their filings. Baby steps....

So Who Actually Owns the Ordinary/ADS Shares?

Executive Summary:

1.) ADS Shares at US Financial Institutions have ballooned from 196 million four years ago to 1.669 Billion now. Per the 20-F these shares are concentrated in 128 US Financial Institutions held in "street name".

2.) A significant number of the shares in US Institutions are held by Chinese insiders through Offshore Shell Companies. 450 Million shares are held by the largest 20 Institutions.

3.) The Chinese Communist Party (CCP) is manipulating the bid/ask through myriad offshore entities on a relatively small population of "arms length" trades in order to create the illusion of a market made at a price that defies financial gravity. The risk of collapse grows larger by the day.

The statement on page 188 of the 20-F is illuminating:

As of July 18, 2018, 2,592,184,258 of our ordinary shares were outstanding. To our knowledge, 1,669,625,497 ordinary shares, representing approximately 64% of our total outstanding shares, were held by 128 record shareholders with registered addresses in the United States, including brokers and banks that hold securities in street name on behalf of their customers. We are not aware of any arrangement that may at a subsequent date, result in a change of control of our company.

Authors Note: Why in the world did they pick Wednesday July 18th 2018 as the date to disclose the ordinary shares outstanding? My guess would be that they wanted a date that was not comparable to any public filing date so these numbers would be impossible to validate/verify. A Wednesday in the middle of July sounded like a good day to "make shit up".

The 20-F, in the table on pg. 187, with a little bit of "Enhancement" math, shows us the distribution of these shares (One (1) Ordinary Share equals one (1) ADS (American Depository Share)):

When we look at the table above we see that there's an "Overlap". Roughly 455 million shares must be in two places. Presumably, some of Altaba's (Yahoo!) shares, plus a hundred million (or so) shares held by, for example, offshore (Caymans/BVI) shells, in "street name" at the 128 identified US Financial Firms/Brokerages/Banks, are in both places. (Remember how Softbank "sold" some BABA shares to West Raptor Holdings? Yet they are still beneficially owned?) I guess that the "Overlap" might make at least some sense in an odd sort of way.

So now, let's compare that to where we were back in 2014, Post IPO (pg. 250 thru 254 of the 424(b)4 filing)

The statement on page 254 of the filing is illuminating:

As of August 31, 2014, 196,373,235 of our outstanding ordinary shares were held by shareholders of record in the United States, principally Yahoo. We are not aware of any arrangement that may at a subsequent date, result in a change of control of our company.

So let's restate the 2014 - POST IPO figures to compare to the schedule above. The chart below describes how the ownership of BABA would look right after the IPO:

Now let's focus on the "Other Ordinary Shareholders" above. US "Shareholders of Record" have increased from 196 Million shares (8% of Outstanding Shares) immediately after the IPO to 1,669 Million shares (64%) today. Put another way, immediately after the IPO, 30% (745 Million) BABA shares were held outside the US (presumably) by Non-US shareholders in China. It would seem that Jack, Joe, Softbank, Altaba, Officers, Directors and insiders as a group (through offshore shells in "street name") have moved the lions-share of the custodial relationship(s) to US Financial Institutions, where, just thinking out loud, they can pledge these shares as collateral and do all sorts of wonderful "leveragey" things with them. The faith that they've shown in the US Financial System is gratifying and extraordinary.

Now let's go back to page 250 of the 2014 IPO Document (424(b)4 Filing). At the time, we can see below that there were roughly 190 Million shares held by Caymans/BVI Shell Corps.

The following Shell Corps. were listed in the notes as shareholders:

Interestingly, when we do PDF searches of the recent 20-F, the sixty-one (61) entities listed above and apparently integral to the pre-IPO financing structure, we see that these entities are either nonexistent or listed in the periphery today, like, for example, the benign discussion of Jack's "Relationship With Investment Funds" (Pg. 204)

My guess would be that these businesses and their relationships with Alibaba are far from over. These Shells, and probably many more like them, most likely continue to spearhead the proliferation and ADS price management of the Ordinary Shares into the US Financial System. I've described this phenomenon as "Boomerang Money" in prior posts.

Next, let's take a look at the most current 13-F Summary information available on Yahoo! Finance, apply a few ratios, and compare it to the Alibaba 20-F disclosures.

A few things jump off the page at us:

Moreover, do any of you readers remember "Re-Hypothecation"? The practice where banks and brokerages use their customer/client collateral as their own? Let's lever up and hit the gas? Oh sure you remember this.....it's what caused the liquidity crisis that threw Lehman Brothers into bankruptcy.....is it coming back to you now? Could anything like this be happening here?....food for thought.

So who's right? The BABA 20-F Filing (1.6 Billion shares in 128 US Institutions) or Yahoo! Finance's analysis of the 13-F Filings? (1.1 Billion shares held at 1,926 Institutions).

There's a good chance that both might be correct. It could be that there was a massive increase in shares held by US Institutions in the last 6 months. It could be that the insider owned Shells have been going absolutely bonkers....moving more than 600 million shares into US Institutions and consolidating them down from 1,926 banks/brokerages to just 128 in the same time frame. You'd think that BABA management should be very accurate (down to the share) in their filings. You'd also think that Yahoo! Finance is also generally pretty accurate at tabulating 13-F data. They don't usually make mistakes either.

So here's my thesis re: Alibaba's Capital Structure:

Is it possible that, like the RMB, the CCP has opened the same playbook, manipulating the bid/ask through myriad offshore entities on a small population of trades in order to create the illusion of a market made at a price that defies financial gravity? A team of Chinese Communist Party (CCP) Members in the Caymans is relentlessly trading, coordinated with other teams of CCP Members in the BVI, all pitted against a smattering of tidal-chart-watching, butterfly-correlation-coefficient following, nearly retired, fund managers, day traders and self-proclaimed "Seeking Alpha" financial wizards, as the US custodial "street name" share count increases geometrically? Boatloads of these shares continue to find their way onto the books of US Institutions. At some point the 20-F might actually (accidentally) proclaim that there are indeed more shares on deposit in US Financial Institutions than are actually issued/outstanding, in yet another BABA-esqe feat of financial prestidigitation to look forward to!

Financial Comedy Genius!....Kudos!.....Bravo! Like a George Lucas franchise, just when you thought it couldn't possibly get any better, they come up with the financial equivalent of "Jar Jar Binks".

It's a page turner...it has to be....it's 233 pages with an additional 93 pages of circular footnotes, charts and tables, laden with nonsensical, legal sounding gibberish that would make a Securities Lawyer blush with envy and/or question his virility. I've spent the last few evenings going through it (I have a day job...) and I have to say, I couldn't put it down. It's riveting.

Sadly, in this issue, they've left out the family photos, advertising and screen shots of the fake/knock-off products they sell, presumably to save some space. My guess is that some dull-as-a-butter-knife PWC accountant probably talked them out of including the personal, Horatio Alger scrap-book stuff. It's a shame really.

So let's start with the press release......it sets the tone:

The company aims to build the future infrastructure of commerce. It envisions that its customers will meet, work and live at Alibaba, and that it will be a company that lasts at least 102 years.

https://www.businesswire.com/news/home/20180727005591/en/

Yup....that's right....they are guaranteeing that the company will be around not 100 years, not 101 years.....but at least 102 Years! Alibaba will be my (our) life....Alibaba is where we will live, work, meet and eventually be buried.....we'll raise our kids there and our pets will poop on our little slice of heaven that is the Alibaba front lawn. Kind of creepy if you ask me.

As an aside...why aren't they issuing 102 year bonds to show their confidence in the business model?

As always, for your convenience, and because I value your time, feel free to read the RED Executive Summary at the beginning of each section. If the topics don't pique your curiosity, you can move along to the next section and the next Executive Summary as the spirit moves you.

The Capital Structure...(Now you see it....now you don't...)

Executive Summary: In this section we explore the following observations:

1.) There are now 920 separate operating entities in the Alibaba ecosystem. 500 in the PRC and 420 scattered all over the rest of the planet. Alibaba has created 300 new "legal" entities a year for the last two years.

2.) They've "Enhanced" their Capital Structure. The lawyers have been busy beavers.

3.) Major Business Segments and Operating Entities appear and disappear from the 20-F's. There is no explanation in the footnotes.

So where do we start? As you my readers know, I like to jump into really, really important, seemingly innocuous documents (Like Chinese 20-F's) which most people, without a ton of effort, generally can't begin to understand. By virtue of this lack of understanding, they (understandably) don't seem to care too much about these documents until there's a painful enlightenment smacking them in the face somewhere down the road....followed by a chorus of "if only I'd understood this!" and the consequent, requisite Congressional hearings focusing on "blame delegation". That's where I try to add value. I try to help good folks like you, my cherished readers, see what's just over the horizon. As always, I'm here to help.

So, speaking of "things we can't begin to understand without putting in a ton of effort" let's start out by talking about Alibaba's Capital Structure......I know, I know.....stop jumping up and down with glee....try to contain yourselves. It's just accounting.....Geez....

So like we always do with an Alibaba 20-F review, with absolutely no rhyme nor reason, let's pick a random page.....let's start on page.....Oh....I don't know.....how about page 115?

It starts off with some some wonderfully amazing information:

As of March 31, 2018, we conducted our business operations across approximately 500 subsidiaries and consolidated entities incorporated in China and approximately 420 subsidiaries and consolidated entities incorporated in other jurisdictions.

That's right, Alibaba now has 920 Separate Operating Entities! Over the last two years Alibaba has created, out of thin air, or acquired, roughly 300 material Operating Companies per year. That's roughly 600 new businesses, one new company every business day for two years. The Alibaba lawyers have been working a ton of overtime. They must be exhausted.

Let's pause for a moment of silence.....in solemn gratitude.....for the lawyers.

Moving along, Exhibit 8.1 (Ref: on Pg 231) lists "Significant Subsidiaries & Consolidated Entities". There are forty-six (46) businesses apparently deemed to be significant. Sixteen (16) of these businesses are located in the PRC (China), Twelve (12) in the Caymans, Nine (9) in the BVI, Six (6) in Hong Kong, Two (2) in Singapore and finally, One (1) in Luxembourg.

https://www.sec.gov/Archives/edgar/data/1577552/000104746918005257/a2235254zex-8_1.htm

So, I guess, by definition, the remaining 874 businesses (920 - 46) are "insignificant"?

When we drill down a little farther we see that there are really only fifteen (15) businesses that I'll call "Super Significant" (See the Chart on Pg. 115 below)

And of these fifteen (15) "Super Significant" businesses, three (3) of them are brand spanking new in the last fiscal year! And what's really weird, is that Zhejiang Cainiao Supply Chain Co., Ltd., Youku Internet Technology and Youku Information Technology aren't even on the list of "Significant Subsidiaries & Consolidated Entities". (Exhibit 8.1) Is it a typo? So maybe they are not Significant? Just "Super Significant". Puzzling to say the least....

Zhejiang Cainiao Supply Chain Co., Ltd. is only mentioned once in the report, on page 91 under "Regulation of Foreign Investment"

The only time Youku Internet Technology is mentioned in the report is on pg 119 as a party to a contract that "Gives us Control over VIE's". Youku Information Technology is not mentioned at all....here's the ridiculous language re: Youku Internet Technology....

The parties to the loan agreement for each of our material variable interest entities are Jack Ma and Simon Xie or other shareholders of those entities (in respect of the existing VIE structure) or, following the VIE Structure Enhancement, the relevant PRC investment holding company, on the one hand, and Taobao (China) Software Co., Ltd., Zhejiang Tmall Technology Co., Ltd., Alibaba (China) Technology Co., Ltd., Zhejiang Alibaba Cloud Computing Ltd. and Youku Internet Technology (Beijing) Co., Ltd., the respective wholly-foreign owned enterprise, on the other hand.

Forget for a moment that there are now oodles of undisclosed/un-described loan agreements all over the planet with insiders, which is frightening enough, now, on one hand (or the other) we have three new "Significant" businesses, we know nothing about, that have somehow just shown up in the filings this year, that are somehow being "Enhanced".

Let's dig a little further.

When we look at last years (20-F YE 3/31/17 pg. 111) chart we see that Alibaba.com Limited (Caymans) and Alibaba.com Investment Holding Limited (BVI) are both missing from this year's chart, yet they are still included on Exhibit 8.1. A text search of the pdf shows that, oddly enough, the only other time they are mentioned in the filing is in the biography of Walter Kwauk. So where did these "Significant" businesses go? Are they still relevant?

Walter Teh Ming KWAUK (

Since Mr. Kwauk is on the Alibaba Board, and is, in fact, the head of the Alibaba (BABA) audit committee and amazingly "satisfies the criteria of an audit committee financial expert as set forth under the applicable rules of the SEC" (Pg. 184) perhaps, with all of this expertise, he can tell us why the hell these two businesses were removed from the Alibaba Org chart? ....or maybe help us figure out what the three brand-spanking-new businesses that just showed up actually are?

VIE Structure "Enhancement"

Everyone pretty much understands the structure of the Alibaba ecosystem. In broad brush, general terms, it's a group of 36 "partners" listed on page 176 of the filing, who are charged with the responsibility of scouring the world for cash.

Through a convoluted web of dubious financial entities (now 920 in number), designed to meet the legal requirements of Chinese "ownership" and un-auditability, the partners, after careful deliberation, vote to piss away the money raised on kickbacks and political payoffs, in exactly the direction Jack and the CCP tell them to piss it, adjusting for wind, as needed.

Now, you'd think that this would be a pretty easy (and fun) set of marching orders to follow, but over time, we all know how confusing, off-track and complex financial shenanigans can get. Fortunately, last year, Alibaba's lawyers finally grabbed the bull by the horns and undertook a massive effort to simplify Alibaba's capital structure. So let's see what they did, keeping in mind that there are 920 entities in the BABA ecosystem now, with 420 "offshore", mostly located (presumably) in Hong Kong, the Caymans and BVI.

On pg. 116 of the filing, management describes the "VIE Structure Enhancement". This is the summary (in actual English "words") of what they were doing....followed by a "simple" diagram.

Upon the completion of the VIE Structure Enhancement for each VIE, the equity interest of each such variable interest entity will, instead of being held by a few individuals, be directly held by a PRC limited liability company, which in turn will be indirectly held (through a layer of PRC limited partnerships) by selected members of the Alibaba Partnership or our management who are PRC citizens. This new structure institutionalizes the governance framework of our VIEs.

Isn't that Awesome (and really smart sounding)! The diagram below describes how the legal structure of the Variable Interest Entities looked BEFORE the "Enhancements" got underway.

Pretty simple huh?

1.) BABA owns WFOE's through offshore shells (Cayamans/BVI/HK)

2.) The WFOE's secure contracts, "call options" and various agreements with both the VIE's and the VIE shareholders in exchange for loans/cash.

After the "Enhancement" here's what we have.....on pg. 118....much simpler...

After the "Enhancement"....

1.) BABA owns WFOE's through offshore shells (Cayamans/BVI/HK).

2.) The WFOE's enter into contracts and agreements with the VIE's.

3.) Each VIE is owned by a PRC Investment Holding Company.

4.) The PRC Investment Holding Company is owned by various Limited Partnerships.

5.) The Limited Partnerships are owned by Individual Limited Partners and various PRC LLCs as General Partners.

6.) The General Partner LLC is owned by individual shareholders and/or PIE's (Political Insider Elite's).

7.) The WFOE's negotiate contracts and agreements in exchange for loans/cash with ALL of the above entity types.

8.) Again, there are now 920 entities involved in the Alibaba ecosystem and I'd suspect that the number will be growing geometrically.

I, for one, am so glad that Alibaba management has finally acknowledged, through this new Capital Structure "Enhancement", their obligation to be forthright and transparent in their filings. Baby steps....

So Who Actually Owns the Ordinary/ADS Shares?

Executive Summary:

1.) ADS Shares at US Financial Institutions have ballooned from 196 million four years ago to 1.669 Billion now. Per the 20-F these shares are concentrated in 128 US Financial Institutions held in "street name".

2.) A significant number of the shares in US Institutions are held by Chinese insiders through Offshore Shell Companies. 450 Million shares are held by the largest 20 Institutions.

3.) The Chinese Communist Party (CCP) is manipulating the bid/ask through myriad offshore entities on a relatively small population of "arms length" trades in order to create the illusion of a market made at a price that defies financial gravity. The risk of collapse grows larger by the day.

The statement on page 188 of the 20-F is illuminating:

As of July 18, 2018, 2,592,184,258 of our ordinary shares were outstanding. To our knowledge, 1,669,625,497 ordinary shares, representing approximately 64% of our total outstanding shares, were held by 128 record shareholders with registered addresses in the United States, including brokers and banks that hold securities in street name on behalf of their customers. We are not aware of any arrangement that may at a subsequent date, result in a change of control of our company.

Authors Note: Why in the world did they pick Wednesday July 18th 2018 as the date to disclose the ordinary shares outstanding? My guess would be that they wanted a date that was not comparable to any public filing date so these numbers would be impossible to validate/verify. A Wednesday in the middle of July sounded like a good day to "make shit up".

The 20-F, in the table on pg. 187, with a little bit of "Enhancement" math, shows us the distribution of these shares (One (1) Ordinary Share equals one (1) ADS (American Depository Share)):

When we look at the table above we see that there's an "Overlap". Roughly 455 million shares must be in two places. Presumably, some of Altaba's (Yahoo!) shares, plus a hundred million (or so) shares held by, for example, offshore (Caymans/BVI) shells, in "street name" at the 128 identified US Financial Firms/Brokerages/Banks, are in both places. (Remember how Softbank "sold" some BABA shares to West Raptor Holdings? Yet they are still beneficially owned?) I guess that the "Overlap" might make at least some sense in an odd sort of way.

So now, let's compare that to where we were back in 2014, Post IPO (pg. 250 thru 254 of the 424(b)4 filing)

The statement on page 254 of the filing is illuminating:

As of August 31, 2014, 196,373,235 of our outstanding ordinary shares were held by shareholders of record in the United States, principally Yahoo. We are not aware of any arrangement that may at a subsequent date, result in a change of control of our company.

So let's restate the 2014 - POST IPO figures to compare to the schedule above. The chart below describes how the ownership of BABA would look right after the IPO:

Now let's go back to page 250 of the 2014 IPO Document (424(b)4 Filing). At the time, we can see below that there were roughly 190 Million shares held by Caymans/BVI Shell Corps.

The following Shell Corps. were listed in the notes as shareholders:

Interestingly, when we do PDF searches of the recent 20-F, the sixty-one (61) entities listed above and apparently integral to the pre-IPO financing structure, we see that these entities are either nonexistent or listed in the periphery today, like, for example, the benign discussion of Jack's "Relationship With Investment Funds" (Pg. 204)

My guess would be that these businesses and their relationships with Alibaba are far from over. These Shells, and probably many more like them, most likely continue to spearhead the proliferation and ADS price management of the Ordinary Shares into the US Financial System. I've described this phenomenon as "Boomerang Money" in prior posts.

Next, let's take a look at the most current 13-F Summary information available on Yahoo! Finance, apply a few ratios, and compare it to the Alibaba 20-F disclosures.

A few things jump off the page at us:

- First, we see that Yahoo! Finance shows that there are 1,926 US Institutions holding Alibaba Shares as of 12/31/17, rather than the 128 Institutions listed in the 20-F as of 7/18/18. Quite a disparity.

- Yahoo Finance shows 1.051 Billion Shares held by Institutions (rather than 1.669 Billion per the 20-F). Again, quite a difference

- Float, or unrestricted shares available to trade was 1.214 Billion shares, or 46.85% of outstanding shares per Yahoo! Finance. So apparently "Float", at that time was significantly less that the 1.669 Billion shares held by US Institutions today? Are some of these shares still restricted? Unless I'm misinformed, I thought the "Lockups" had long passed.

- Roughly 40% of float, as of 12/31/17 was concentrated in twenty (20) US institutions.

Moreover, do any of you readers remember "Re-Hypothecation"? The practice where banks and brokerages use their customer/client collateral as their own? Let's lever up and hit the gas? Oh sure you remember this.....it's what caused the liquidity crisis that threw Lehman Brothers into bankruptcy.....is it coming back to you now? Could anything like this be happening here?....food for thought.

So who's right? The BABA 20-F Filing (1.6 Billion shares in 128 US Institutions) or Yahoo! Finance's analysis of the 13-F Filings? (1.1 Billion shares held at 1,926 Institutions).

There's a good chance that both might be correct. It could be that there was a massive increase in shares held by US Institutions in the last 6 months. It could be that the insider owned Shells have been going absolutely bonkers....moving more than 600 million shares into US Institutions and consolidating them down from 1,926 banks/brokerages to just 128 in the same time frame. You'd think that BABA management should be very accurate (down to the share) in their filings. You'd also think that Yahoo! Finance is also generally pretty accurate at tabulating 13-F data. They don't usually make mistakes either.

So here's my thesis re: Alibaba's Capital Structure:

Is it possible that, like the RMB, the CCP has opened the same playbook, manipulating the bid/ask through myriad offshore entities on a small population of trades in order to create the illusion of a market made at a price that defies financial gravity? A team of Chinese Communist Party (CCP) Members in the Caymans is relentlessly trading, coordinated with other teams of CCP Members in the BVI, all pitted against a smattering of tidal-chart-watching, butterfly-correlation-coefficient following, nearly retired, fund managers, day traders and self-proclaimed "Seeking Alpha" financial wizards, as the US custodial "street name" share count increases geometrically? Boatloads of these shares continue to find their way onto the books of US Institutions. At some point the 20-F might actually (accidentally) proclaim that there are indeed more shares on deposit in US Financial Institutions than are actually issued/outstanding, in yet another BABA-esqe feat of financial prestidigitation to look forward to!

All that said, the big hypothetical question is, what happens when the CCP decides to hit the "sell" button?

1.) In the last year Alibaba has added roughly "Fifteen Pentagons" in office space with only 16,000 additional FTE's, or roughly 3,400 new square feet per new employee. Real Estate is expensive, yet, overhead stayed about the same. Weird.....

2017 20-F Pg 115

As of March 31, 2017, we occupied facilities around the world with an aggregate gross floor area of office buildings owned by us totaling 558,080 square meters. (6,007,173 square feet)

2018 20-F Pg 121

As of March 31, 2018, we occupied facilities around the world with an aggregate gross floor area of office buildings owned by us totaling approximately 5.7 million square meters. (61,354,800 square feet.)

(Authors Note: Whooooaaaa!!! 61 million square feet of OFFICE BUILDINGS OWNED by Alibaba!!!???)

2018 20-F Pg 121

As of March 31, 2016, 2017 and 2018, we had a total of 36,446, 50,097 and 66,421 full-time employees, respectively.

As a point of reference, the US Pentagon, I'm told, is the world's largest office building, with about 6,500,000 sq ft (600,000 m2), of which 3,700,000 sq ft (340,000 m2) are used as offices. The Pentagon houses roughly 26,000 Office Employees.

Taking the analysis a step further, since the US Government has been long renowned as the world's foremost efficiency expert, using the appropriate Pentagon ratios, we can calculate that 61,354,800 square feet of office space (the world's biggest cube farm) would accommodate 430,711 employees, each of whom would be allotted 142 square feet of gross office space.

Executive Summary:

1.) Alibaba has a retail presence roughly 1.5 x Walmart now. GMV is US$ 768 Billion vs. Walmarts piddling US$ 500 Billion.

2.) BABA has developed a huge new revenue stream, winding down the huge, and rapidly growing supply of China's Non-Performing Loans (NPLS), yet, this business segment wasn't mentioned in the 20-F at all.

3.) Based on the value of "real" retail GMV the Market Cap of Alibaba should be about the same as Target (NYSE:TGT) (US$ 40 Billion) rather than US$ 470 Billion, the company's current Market Cap.

The increase was primarily due to a non-cash gain of RMB22,442 million (US$3,578 million) arising from the revaluation of our previously held equity interest in Cainiao Network when we acquired control over Cainiao Network in mid-October 2017.

It is indeed fortuitous that wonderful write-up opportunities like Cainiao pop up just when a businesses like Alibaba Pictures begin to falter. Alibaba management is truly blessed.

The obvious question I have is, the total gain booked is US$4.137 Billion (Pg. 4) and that includes the Cainiao gain of US$3.578 Billion that would indicate that there's another US$559 Million in write ups that are not described anywhere else. In a mainland investment environment where equities are down substantially in the last six months, could it be that these write ups might be illusory and there are more write-downs/offs on the horizon?

Wanda - Note 4(k) F-52

Wanda Film, a company that is listed on the Shenzhen Stock Exchange, is principally engaged in the investment and management of cinemas and film distribution businesses. In March 2018, the Company completed an investment in existing ordinary shares of Wanda Film for a cash consideration of RMB4,676 million, representing an approximately 8% equity interest in Wanda Film. Such investment is accounted for under the cost method (Note 13) given that a readily determinable fair value is not available due to the suspension of trading of its shares for an extended period as of March 31, 2018.

This was a really shrewd move, showing the brilliance of Alibaba management, as well as their benevolence, helping Xi's buddy, Wang Jianglin out of a real jam since trading had been suspended for nearly a year (since July 4th, 2017) at the time of the Alibaba "investment" . Alibaba was able to swoop in and pick up this stock at a bargain price while it was suspended/pending-de-listed. Also, thanks to the generous nature and unwavering faith of US Shareholders, Alibaba management knew full well that there would be no repercussions from failing to book the US$750 Million write off/down and burying this transaction in a one paragraph disclosure deep in the bowels of the footnotes of the 20-F. As we all know, in China, suspension of trading, or even better, a de-listing is a vote of confidence for management and validates a businesses intrinsic value. It's a confirmation that management has everything under control. (For you Chinese readers out there, that was what we Westerners refer to as "sarcasm".)

OFO Bike Sharing (F-52)

(m) Investment in OFO International Limited ("OFO")

OFO is one of the leading bike-sharing companies in the PRC. During the year ended March 31, 2018, the Company completed an investment in existing and newly issued preferred shares of OFO for a total cash consideration of US$343 million (RMB2,272 million). As of March 31, 2018, the Company's equity interest in OFO was approximately 12% on a fully diluted basis. Ant Financial is also an existing minority shareholder of OFO. Such investment is accounted for under the cost method (Note 13).

https://www.forbes.com/sites/bizcarson/2018/07/18/ofo-bikes-us/#78fed8872785

This picture pretty much says it all.....I'm sure everything is just fine and dandy at OFO.

Employees and their Office Space!

Executive Summary:

Executive Summary:

1.) In the last year Alibaba has added roughly "Fifteen Pentagons" in office space with only 16,000 additional FTE's, or roughly 3,400 new square feet per new employee. Real Estate is expensive, yet, overhead stayed about the same. Weird.....

2017 20-F Pg 115

As of March 31, 2017, we occupied facilities around the world with an aggregate gross floor area of office buildings owned by us totaling 558,080 square meters. (6,007,173 square feet)

2018 20-F Pg 121

As of March 31, 2018, we occupied facilities around the world with an aggregate gross floor area of office buildings owned by us totaling approximately 5.7 million square meters. (61,354,800 square feet.)

(Authors Note: Whooooaaaa!!! 61 million square feet of OFFICE BUILDINGS OWNED by Alibaba!!!???)

2018 20-F Pg 121

As a point of reference, the US Pentagon, I'm told, is the world's largest office building, with about 6,500,000 sq ft (600,000 m2), of which 3,700,000 sq ft (340,000 m2) are used as offices. The Pentagon houses roughly 26,000 Office Employees.

So in just one (1) year Alibaba has increased their office space the equivalent of fifteen (15) Pentagons? That's amazing! So I guess real estate expense & overhead should be going up a bit??.....

I also understand that they just redid the bathrooms and put in new Berber carpet at their World-Wide Global Headquarters in the Caymans (Alibaba Group Holding Limited, Trident Trust Co (Cayman) Ltd, One Capital Place 4th Floor, Georgetown, Cayman). Gorgeous! Ain't she a beauty? Money is apparently no object.

I also understand that they just redid the bathrooms and put in new Berber carpet at their World-Wide Global Headquarters in the Caymans (Alibaba Group Holding Limited, Trident Trust Co (Cayman) Ltd, One Capital Place 4th Floor, Georgetown, Cayman). Gorgeous! Ain't she a beauty? Money is apparently no object.

Taking the analysis a step further, since the US Government has been long renowned as the world's foremost efficiency expert, using the appropriate Pentagon ratios, we can calculate that 61,354,800 square feet of office space (the world's biggest cube farm) would accommodate 430,711 employees, each of whom would be allotted 142 square feet of gross office space.

When we compare this to Alibaba's space usage we see that even though they've added "15 Pentagons" of Office Space, they've only added 16,324 FTE's. This would give each new employee roughly 3,390 sq. ft. of new lounging area . Spacious indeed! No wonder everyone wants to work at Alibaba.!

Moreover, when we look at the book value of the newly acquired "15 Pentagons" we see that the new space doesn't seem to be nearly as luxurious as the currently owned space. When we compare the Balance Sheet values of Property & Equipment (net of depreciation) for 2018 and 2017 (F-5 of the respective 20-F's) we see that the Book Value per square foot, including the newly added 55 million square feet of space drops from $488.75 per square foot down to $172.77. Since the bulk of the 2018 $10.6 Billion is newly acquired space with presumably very little depreciation, it looks like Alibaba, as always got an incredible deal!

Since these numbers are so cattywampus a schedule showing the addresses of major buildings, their square footage and cost basis would have been appreciated.

Since these numbers are so cattywampus a schedule showing the addresses of major buildings, their square footage and cost basis would have been appreciated.

Moreover, when we look at the book value of the newly acquired "15 Pentagons" we see that the new space doesn't seem to be nearly as luxurious as the currently owned space. When we compare the Balance Sheet values of Property & Equipment (net of depreciation) for 2018 and 2017 (F-5 of the respective 20-F's) we see that the Book Value per square foot, including the newly added 55 million square feet of space drops from $488.75 per square foot down to $172.77. Since the bulk of the 2018 $10.6 Billion is newly acquired space with presumably very little depreciation, it looks like Alibaba, as always got an incredible deal!

GMVVVVVVVVV!

Executive Summary:

1.) Alibaba has a retail presence roughly 1.5 x Walmart now. GMV is US$ 768 Billion vs. Walmarts piddling US$ 500 Billion.

2.) BABA has developed a huge new revenue stream, winding down the huge, and rapidly growing supply of China's Non-Performing Loans (NPLS), yet, this business segment wasn't mentioned in the 20-F at all.

3.) Based on the value of "real" retail GMV the Market Cap of Alibaba should be about the same as Target (NYSE:TGT) (US$ 40 Billion) rather than US$ 470 Billion, the company's current Market Cap.

Gross Merchandise Volume (GMV) has long been a favorite topic of discussion for Alibaba watchers, even though it seems to have evolved into a much less important management metric over the last few years. It's only disclosed annually (and once on "Singles Day") now. (For Example: In the IPO filing "GMV" was mentioned 223 times, while in this years 20-F it was mentioned just 29 times, most of the references were related to the table on page 7 described below).

The supposition by most of us is that Alibaba can't possibly be selling anywhere near the amount of socks, underwear, winter coats, TV's and phones, etc. that they purport to sell. They've never disclosed anything close to a "product mix" analysis for their GMV. Of course there have been all sorts of anecdotes and funny stories about how Alibaba sells boatloads of Yachts, Bad-Assets, Auctioned NPL's, Skyscrapers, Estonian Real Estate and Jumbo Jets.

We are told often by Alibaba management that they continue to be ever vigilant and on the lookout for knock-offs and fakes, even though a third grader with an iPhone can come up with pages of questionable SKU's instantly by typing "Gucci" or "Prada" in a T-Mall or Taobao search box. Jack, for all of his effort, assurances and representations, apparently doesn't have his best men/women on it....

There's also some excellent research, sent to me by one of my readers, done by the Paulsen Institute and Marco Polo, which makes a solid attempt to quantify at least some of this silliness. Apparently, winding down the ever growing basket of China's non-performing loans (NPL's) has become a significant part of the Alibaba business model. Here are a few bullet points from the July 25th, 2018 article:

- Alibaba, through its Taobao platform, has assumed a uniquely broad role in helping China’s financial sector extract value from bad loans.

- Taobao has the potential to become the single most important platform for NPL auctions. In 4Q 2017 NPLs with a face value of 33 billion yuan (US$ 5.3 Billion) were auctioned on Taobao.

- Meanwhile, Taobao has become the judicial system’s platform of choice, with some 3,500 courts throughout China currently using it for judicial auctions.

For some reason, this new, high-growth aspect of Alibaba's business model (US$20+ Billion on an annualized run rate) wasn't mentioned anywhere in the 20-F or during the Investor Call. Strange....

All that said, according to their numbers, Alibaba now controls more GMV in their ecosystem than Walmart's global merchandise sales. Here are the numbers.

Alibaba's GMV is now US$768 Billion (RMB 4,820B/6.276) (2018 20-F Pg. 7) Compared to Walmart's meager $500 Billion in Revenue. Again, in just a few short years Alibaba has grown its GMV retail presence to 150%+ of Walmart's global revenue. BABA GMV is up nearly 3x from the $296 Billion it reported at the time of the IPO.

Of course, there are all sorts of estimates and guesses out there that "real" retail GMV is probably about a third, or half of what they've reported, but that doesn't seem to bother investors. US Investors are willing to shell out hard earned dollars to get in on the ground floor of this China eCommerce dream. When I mention the GMV issues, BABA boosters will often come back with "yeah....the books are probably cooked....but it doesn't matter, the business model is solid.....that's just the way it is in China!"

Here's the "simple math" as to why it does indeed matter. Let's say that Alibaba's GMV is actually 1/3rd of what it's reporting (humor me here) and that the rest of the GMV actually is overstatements, returns, puffing, bad assets, kickbacks, balance transfers, NPL's and low margin/value transactions not necessarily associated with retail/eCommerce. So BABA's "Retail Presence" drops from US$768 Billion down to US$ 256 billion. BABA is, of course, valued as an ECommerce Retailer based on their market presence. You'd think that Business (A) with a third of the market presence of a similar Business (B) would be worth much less.

Further, let's look at the RMB/USD Exchange Rate (See how this is all related??) From my prior posts we can conclude with a SWAG that the Exchange Rate is also overstated by a factor of three (3), which would further reduce the US$ value of Alibaba's "Retail Presence" from US$256 Billion down to US$85 Billion. As a point of reference, Target's Revenue is $72 Billion with a Market Cap of US$ 40 Billion. Alibaba's current Market Cap is just shy of US$470 Billion.

I'm feeling a bit of a valuation disconnect here.

Further, let's look at the RMB/USD Exchange Rate (See how this is all related??) From my prior posts we can conclude with a SWAG that the Exchange Rate is also overstated by a factor of three (3), which would further reduce the US$ value of Alibaba's "Retail Presence" from US$256 Billion down to US$85 Billion. As a point of reference, Target's Revenue is $72 Billion with a Market Cap of US$ 40 Billion. Alibaba's current Market Cap is just shy of US$470 Billion.

I'm feeling a bit of a valuation disconnect here.

"Investees" (More Preseidigitation!)

Executive Summary

1.) We examine Footnote 4 of the 20-F where we see that Book Values (Cost Basis plus write-ups) of Investees have increased roughly US$22.3 Billion in the current year.

2.) A number of former "Flagship" businesses (Auto Navi, UC Web, OneTouch, Singapore Post, Weibo, Meizu) are all missing in action. They've disappeared without a trace or mention in the 20-F.

3.) Consolidating money-losing-dog-shit businesses using all sorts of valuation shenanigans to hide what's happening, and/or bailing out friends with US Shareholder Money seems to have consumed much of management's time and resources.

4.) We examine the footnotes for Alibaba Pictures, Cainiao, Wanda, OFO, Alibaba Health and Wasu. These are AWESOME!!

When we examine Footnote 4 (one of my favorite footnotes) this year a few things jump out at us. But before we get into the nitty-gritty I'd like to take a moment to congratulate the Alibaba Accounting Department on their continuing effort (similar to their effort to root out fake, knock-off merchandise and Capital Structure "Enhancement") in moving toward complete transparency on their disclosures. I particularly like:

So as of the 2017 year-end 20-F Alibaba had "invested" US$ 33.903 Billion in these businesses and booked US$ 7.299 Billion in valuation gains "Life to date". Good. Got it. Now, fast forward to this year's 20-F.

Interestingly, in this year's 20-F the only place the aggregate "Gain on Deemed Disposals of Assets" of US$ 4.137 Billion is mentioned is on page 4 in the "Reconciliation of Net Income to Non-GAAP Income". If it were me, I would have put together a schedule prominently describing the composition of this gigantic figure and what businesses/disposals it relates to, especially since it represents roughly a third of Non-GAAP Income. But that's just me.

The table below compares the 2018 "Note 4" to the 2017 "Note 4" Investment/Purchase values. Again, note that the "valuation gains" assignable to each Investee are no longer disclosed.

Based on the footnotes, Investments and Commitments (soon to close) in these businesses increased by US$ 22.3 Billion last year.

Based on the footnotes, Investments and Commitments (soon to close) in these businesses increased by US$ 22.3 Billion last year.

Interestingly, we also have a number of new "Investees" that showed up on the Alibaba books this year:

Executive Summary

1.) We examine Footnote 4 of the 20-F where we see that Book Values (Cost Basis plus write-ups) of Investees have increased roughly US$22.3 Billion in the current year.

2.) A number of former "Flagship" businesses (Auto Navi, UC Web, OneTouch, Singapore Post, Weibo, Meizu) are all missing in action. They've disappeared without a trace or mention in the 20-F.

3.) Consolidating money-losing-dog-shit businesses using all sorts of valuation shenanigans to hide what's happening, and/or bailing out friends with US Shareholder Money seems to have consumed much of management's time and resources.

4.) We examine the footnotes for Alibaba Pictures, Cainiao, Wanda, OFO, Alibaba Health and Wasu. These are AWESOME!!

When we examine Footnote 4 (one of my favorite footnotes) this year a few things jump out at us. But before we get into the nitty-gritty I'd like to take a moment to congratulate the Alibaba Accounting Department on their continuing effort (similar to their effort to root out fake, knock-off merchandise and Capital Structure "Enhancement") in moving toward complete transparency on their disclosures. I particularly like:

- That Footnote 4 (Pg. F-36) must be read in conjunction with Footnote 11 (Pg. F-71) and Footnote 13 (Pg. F -76), giving the reader practice in both turning pages and maintaining concentration as he/she tries to figure out what's going on.

- Even though the 20-F is published for US Shareholders, in English, for shares traded on the NYSE, the report presents values, randomly switching between RMB, HK$ and US$, giving the reader the chance to familiarize himself with global exchange rates at various points in time.

- Unlike last year, they've chosen not to report both carrying value of the acquired businesses or "life to date" gains booked associated with the step-acquisitions of individual businesses. Rather than bury them in confusing footnotes they've chosen to omit them all together so the reader doesn't get overwhelmed.

- We had to "back into" the valuation for "Other" (RMB 6,406 Million = US$1.020 Billion)) since management decided to show the change in balances rather than the original Cost/Investment. (RMB 5,292 Million + RMB 834 Million)

- They've added a teeny-tiny paragraph following 2(ag) showing the US$6 Billion of transactions that they've committed to, but haven't quite closed (Focus Media, DSM, ZTO, etc.) over the couple of months since year end. It looks like the spending spree is accelerating.

So as of the 2017 year-end 20-F Alibaba had "invested" US$ 33.903 Billion in these businesses and booked US$ 7.299 Billion in valuation gains "Life to date". Good. Got it. Now, fast forward to this year's 20-F.

Interestingly, in this year's 20-F the only place the aggregate "Gain on Deemed Disposals of Assets" of US$ 4.137 Billion is mentioned is on page 4 in the "Reconciliation of Net Income to Non-GAAP Income". If it were me, I would have put together a schedule prominently describing the composition of this gigantic figure and what businesses/disposals it relates to, especially since it represents roughly a third of Non-GAAP Income. But that's just me.

The table below compares the 2018 "Note 4" to the 2017 "Note 4" Investment/Purchase values. Again, note that the "valuation gains" assignable to each Investee are no longer disclosed.

Interestingly, we also have a number of new "Investees" that showed up on the Alibaba books this year:

Wanda, Easy Home, OFO, Sun Art, Yiguo, China Unicom, Sauche, Best Inc, Tokopedia,

Onshore/Offshore, Focus Media, DSM Group, ZTO, Huitonga, Shiji Retail and Kaiuan. "New" Investments totaled RMB 86.831 Billion (US$13.835 Billion).

Onshore/Offshore, Focus Media, DSM Group, ZTO, Huitonga, Shiji Retail and Kaiuan. "New" Investments totaled RMB 86.831 Billion (US$13.835 Billion).

We also note that a number of Alibaba's flagship investments are missing from Footnote 4:

Auto Navi, Alibaba Pictures, UC Web, OneTouch, Singapore Post, Weibo, InTime, Cainaio, Meizu totaling RMB 45.538 Billion (US$ 7.256 Billion) are missing in action.

PDF searches of the 20-F document reveal that:

Auto Navi, Alibaba Pictures, UC Web, OneTouch, Singapore Post, Weibo, InTime, Cainaio, Meizu totaling RMB 45.538 Billion (US$ 7.256 Billion) are missing in action.

PDF searches of the 20-F document reveal that:

- Auto Navi is discussed 10 times in the boilerplate "for example" language unchanged from the prior year, but there is no discussion of the business. It's a shame, from reading the IPO docs you would have thought this business was one of Alibaba's crowned jewels.

- Alibaba Pictures was removed from Footnote 4 and discussed separately.

- UC Web is no longer referred to as "UC Web". It shows up in the 20-F as "UC Browser". The only current (non-boilerplate) reference in the filing appears on page 81: "UC Browser is one of the top three mobile browsers in the world and the number two mobile browser in India and Indonesia by page view market share in March 2018, according to StatCounter (http://gs.statcounter.com)"

- OneTouch was mentioned once on page 162 under "Allowance for Doubtful Accounts Relating to VAT Receivables". The note was the same as last year, management probably just forgot to remove it from that paragraph. In any case OneTouch has disappeared without a trace.

- The Singapore Post is also gone. We don't know what happened to this great business, at least from the filings.

- Any mention of the RMB 7,310 Million (US$ 1,165 Million) valuation for Weibo is missing in action as well.

- InTime was consolidated following the acquisition of the majority of outstanding shares. (Note: 4(c))

- Cainaio was consolidated (Note: 4(b))

- Meizu's RMB 3,619 Million (US$ 567 Million) valuation has disappeared as well. Perhaps a half-billion-plus dollars is no longer a material amount to Alibaba?

Featured Notes worth discussing:

Alibaba Pictures - Page. 162

After years of delay they've finally written down (and consolidated) Alibaba Pictures, taking an impairment charge of RMB18.116 Billion (US$2.888 Billion). They were also careful to mention on page 162:

Nonetheless, the market value of our investment in Alibaba Pictures as of March 31, 2018 remains well above our original investment amount that we paid in June 2014.

This Alibaba Pictures write down was coincidentally offset by a consolidation gain for the write up of Cainiao, here's the note buried on page 129.

Alibaba Pictures - Page. 162

After years of delay they've finally written down (and consolidated) Alibaba Pictures, taking an impairment charge of RMB18.116 Billion (US$2.888 Billion). They were also careful to mention on page 162:

Nonetheless, the market value of our investment in Alibaba Pictures as of March 31, 2018 remains well above our original investment amount that we paid in June 2014.

This Alibaba Pictures write down was coincidentally offset by a consolidation gain for the write up of Cainiao, here's the note buried on page 129.

In October 2017, as a further step to implement our New Retail strategy, we completed a subscription for newly issued ordinary shares of Cainiao Network for a cash consideration of US$803 million. Following the completion of the transaction, our equity interest in Cainiao Network increased from an approximately 47% to an approximately 51% and Cainiao Network became our consolidated subsidiary. We expect that Cainiao Network will help enhance the overall logistics experience for consumers and merchants across our ecosystem, and enable greater efficiencies and lower costs in the logistics sector in China.

The amount of the gain is buried on page 145.

It is indeed fortuitous that wonderful write-up opportunities like Cainiao pop up just when a businesses like Alibaba Pictures begin to falter. Alibaba management is truly blessed.

The obvious question I have is, the total gain booked is US$4.137 Billion (Pg. 4) and that includes the Cainiao gain of US$3.578 Billion that would indicate that there's another US$559 Million in write ups that are not described anywhere else. In a mainland investment environment where equities are down substantially in the last six months, could it be that these write ups might be illusory and there are more write-downs/offs on the horizon?

Wanda - Note 4(k) F-52

Wanda Film, a company that is listed on the Shenzhen Stock Exchange, is principally engaged in the investment and management of cinemas and film distribution businesses. In March 2018, the Company completed an investment in existing ordinary shares of Wanda Film for a cash consideration of RMB4,676 million, representing an approximately 8% equity interest in Wanda Film. Such investment is accounted for under the cost method (Note 13) given that a readily determinable fair value is not available due to the suspension of trading of its shares for an extended period as of March 31, 2018.

This was a really shrewd move, showing the brilliance of Alibaba management, as well as their benevolence, helping Xi's buddy, Wang Jianglin out of a real jam since trading had been suspended for nearly a year (since July 4th, 2017) at the time of the Alibaba "investment" . Alibaba was able to swoop in and pick up this stock at a bargain price while it was suspended/pending-de-listed. Also, thanks to the generous nature and unwavering faith of US Shareholders, Alibaba management knew full well that there would be no repercussions from failing to book the US$750 Million write off/down and burying this transaction in a one paragraph disclosure deep in the bowels of the footnotes of the 20-F. As we all know, in China, suspension of trading, or even better, a de-listing is a vote of confidence for management and validates a businesses intrinsic value. It's a confirmation that management has everything under control. (For you Chinese readers out there, that was what we Westerners refer to as "sarcasm".)

OFO Bike Sharing (F-52)

(m) Investment in OFO International Limited ("OFO")

OFO is one of the leading bike-sharing companies in the PRC. During the year ended March 31, 2018, the Company completed an investment in existing and newly issued preferred shares of OFO for a total cash consideration of US$343 million (RMB2,272 million). As of March 31, 2018, the Company's equity interest in OFO was approximately 12% on a fully diluted basis. Ant Financial is also an existing minority shareholder of OFO. Such investment is accounted for under the cost method (Note 13).

https://www.forbes.com/sites/bizcarson/2018/07/18/ofo-bikes-us/#78fed8872785

This picture pretty much says it all.....I'm sure everything is just fine and dandy at OFO.

Alibaba Health (F-52 (4(i))

I discussed the recent history of Alibaba Health and Yunfeng (Jack's Piggy Bank) in my analysis of last year's 20-F. Feel free to refresh your memory by rereading the section entitled Alibaba Health ....More of the same.

We see a familiar game plan. Create a fake valuation based on a small piece of the pie and value the entire enterprise based on that piece, as you make "step" acquisitions and book valuation "gains".

In May 2018, the Company agreed to transfer its business relating to certain medical devices, healthcare and adult products and the medical and healthcare services on Tmall to Alibaba Health for an aggregate consideration of HK$10.6 billion, which will be settled through the issuance of approximately 1.8 billion newly issued ordinary shares of Alibaba Health. The completion of this transaction is subject to a number of conditions including the approval by the shareholders of Alibaba Health and certain regulatory authorities. Upon the closing of this transaction, the Company's effective equity ownership of Alibaba Health will increase to approximately 56%.

Since the value of Alibaba Health (HK:241) nearly doubled after the announcement, a statement like this absolutely screams for the deployment of the Banker Speak Translator (BST). Here's what the note really says:

BST: This is AWESOME! we took a bunch of floundering product categories out of TMall that nobody knows the value of, said they were worth HK$ 10.6 Billion and had a company we control (Alibaba Health) issue shares in that amount, increasing the Shareholder Equity in the company without spending a dime of cash! (Shit!....we should have made it HK$20.0 Billion!) And now that we have a 56% ownership interest we can probably just consolidate it and get it off that that pesky Hong Kong stock exchange where uninformed shareholders can "vote" on the value of the business every day and muck up the works.

Maybe I'm over simplifying, but it looks like the only thing that the shareholders of Alibaba Health got for their HK$ 10.6 Billion of dilution is a link on the Alihealth.cn home page redirecting to the Tmall Health page where they can buy all sorts of cheap, questionable medications. Try it....it's kind of funny/lame.

http://www.alihealth.cn/

So here's what Alibaba Health looks like today. Note that the stock nearly doubled since the May announcement that Alibaba was "trading" the TMall health care business for HK$ 10.6 Billion of dilution:

My guess is that they will be consolidating this mess at some point (another valuation gain is on the horizon) and they won't have to discuss the gory details again in next year's 20-F. With the issuance of the HK$ 10.6 Billion new shares, they will have (by my calculations from these footnotes) spent RMB 65.429 Billion (Including the RMB 18.603 valuation gains booked in prior years) to acquire 56% of Alibaba Health. The Market Cap of Alibaba health today is RMB 79.0 Billion (Even after the recent run up....Note that the Market Cap was RMB 40 Billion just prior to the May, 2018 announcement.). A 56% interest in Alibaba Health should be worth about RMB 44.24 Billion now.

I'll be the first to admit that I had a really hard time going through the footnotes and currency conversions in order to do these calculations and I'd appreciate any guidance or help from anyone familiar with this transaction. As an aside, it would have been nice if they just would have disclosed that:

"Our Cost Basis (What we Paid for the business + "write ups") is US$ XXX Billion"

"The current market value (3/31/18) of the 56% of the business we own is US$ YYY Billion"

"We carry the investment at cost so we have an unrealized gain/loss of US$ ZZZ Billion"

Wouldn't that be better than burying all of these step transactions, recapitalizations and valuation changes in the footnotes for the poor, uninformed reader to stumble through and try to decipher?

So after all of the smoke clears, it looks like they've got yet another unrecorded/unrealized loss of RMB 21.189 Billion (US$ 3.854 Billion) at the current market value of Alibaba Health (HK:241), that will have to hit earnings at some point in time.

All of these unrecognized "US$ Billions" of losses are going to start adding up...

Wasu Media (F-58 Note 4(ag))

We covered the incestuous relationship between Wazu Media, Jack and Simon Xie in last year's Finding Inner Peace in Dharamasal 20-F post. I'd encourage you to re-read it.....it's pretty entertaining even if I do say so myself.

In a nutshell, Simon got Jack to spend US$ 1 Billion of US Shareholder's money on "Wealth Management Products" to use as collateral so that an unnamed Chinese banker would make Simon a loan to buy a minority interest in "Wasu Media".

There's no change described in the structure of this absurd deal in this year's 20-F. Simon still owes the US$1 Billion to the unnamed Chinese banker and he's still paying the interest on the loan using the money from his other loan directly from Alibaba. The money drawn on this RMB 2 Billion Line of Credit given to Simon Xie (to pay the interest on the Billion US dollar loan keep this thing afloat) has increased by another RMB 400 Million to RMB 1.137 Billion. So it continues to bleed.

So Alibaba is on the hook for both the principal and interest. Tell me again, one more time, why we need Simon Xie involved?

Here's a summary of how Wasu Media has done since the Spring of 2015 when Simon got his hands on the reins of this juggernaut. Looks like the stock tanked from 60 to 8....Ouch! I'll bet that "unnamed Chinese banker" isn't too happy.

Jay Clayton's SEC

Executive Summary:

The SEC, our best and brightest financial regulator is absolutely, completely OK with everything I've described above. Steady as she goes.....don't want to rock the boat. Jay should be really proud of his trained puppy dogs. "Roll over!...Play dead!....that's such a good boy!"

I discussed the recent history of Alibaba Health and Yunfeng (Jack's Piggy Bank) in my analysis of last year's 20-F. Feel free to refresh your memory by rereading the section entitled Alibaba Health ....More of the same.

We see a familiar game plan. Create a fake valuation based on a small piece of the pie and value the entire enterprise based on that piece, as you make "step" acquisitions and book valuation "gains".

In May 2018, the Company agreed to transfer its business relating to certain medical devices, healthcare and adult products and the medical and healthcare services on Tmall to Alibaba Health for an aggregate consideration of HK$10.6 billion, which will be settled through the issuance of approximately 1.8 billion newly issued ordinary shares of Alibaba Health. The completion of this transaction is subject to a number of conditions including the approval by the shareholders of Alibaba Health and certain regulatory authorities. Upon the closing of this transaction, the Company's effective equity ownership of Alibaba Health will increase to approximately 56%.

Since the value of Alibaba Health (HK:241) nearly doubled after the announcement, a statement like this absolutely screams for the deployment of the Banker Speak Translator (BST). Here's what the note really says:

BST: This is AWESOME! we took a bunch of floundering product categories out of TMall that nobody knows the value of, said they were worth HK$ 10.6 Billion and had a company we control (Alibaba Health) issue shares in that amount, increasing the Shareholder Equity in the company without spending a dime of cash! (Shit!....we should have made it HK$20.0 Billion!) And now that we have a 56% ownership interest we can probably just consolidate it and get it off that that pesky Hong Kong stock exchange where uninformed shareholders can "vote" on the value of the business every day and muck up the works.

Maybe I'm over simplifying, but it looks like the only thing that the shareholders of Alibaba Health got for their HK$ 10.6 Billion of dilution is a link on the Alihealth.cn home page redirecting to the Tmall Health page where they can buy all sorts of cheap, questionable medications. Try it....it's kind of funny/lame.

http://www.alihealth.cn/

So here's what Alibaba Health looks like today. Note that the stock nearly doubled since the May announcement that Alibaba was "trading" the TMall health care business for HK$ 10.6 Billion of dilution:

My guess is that they will be consolidating this mess at some point (another valuation gain is on the horizon) and they won't have to discuss the gory details again in next year's 20-F. With the issuance of the HK$ 10.6 Billion new shares, they will have (by my calculations from these footnotes) spent RMB 65.429 Billion (Including the RMB 18.603 valuation gains booked in prior years) to acquire 56% of Alibaba Health. The Market Cap of Alibaba health today is RMB 79.0 Billion (Even after the recent run up....Note that the Market Cap was RMB 40 Billion just prior to the May, 2018 announcement.). A 56% interest in Alibaba Health should be worth about RMB 44.24 Billion now.

I'll be the first to admit that I had a really hard time going through the footnotes and currency conversions in order to do these calculations and I'd appreciate any guidance or help from anyone familiar with this transaction. As an aside, it would have been nice if they just would have disclosed that:

"Our Cost Basis (What we Paid for the business + "write ups") is US$ XXX Billion"

"The current market value (3/31/18) of the 56% of the business we own is US$ YYY Billion"

"We carry the investment at cost so we have an unrealized gain/loss of US$ ZZZ Billion"

Wouldn't that be better than burying all of these step transactions, recapitalizations and valuation changes in the footnotes for the poor, uninformed reader to stumble through and try to decipher?

So after all of the smoke clears, it looks like they've got yet another unrecorded/unrealized loss of RMB 21.189 Billion (US$ 3.854 Billion) at the current market value of Alibaba Health (HK:241), that will have to hit earnings at some point in time.

All of these unrecognized "US$ Billions" of losses are going to start adding up...

Wasu Media (F-58 Note 4(ag))

We covered the incestuous relationship between Wazu Media, Jack and Simon Xie in last year's Finding Inner Peace in Dharamasal 20-F post. I'd encourage you to re-read it.....it's pretty entertaining even if I do say so myself.

In a nutshell, Simon got Jack to spend US$ 1 Billion of US Shareholder's money on "Wealth Management Products" to use as collateral so that an unnamed Chinese banker would make Simon a loan to buy a minority interest in "Wasu Media".

There's no change described in the structure of this absurd deal in this year's 20-F. Simon still owes the US$1 Billion to the unnamed Chinese banker and he's still paying the interest on the loan using the money from his other loan directly from Alibaba. The money drawn on this RMB 2 Billion Line of Credit given to Simon Xie (to pay the interest on the Billion US dollar loan keep this thing afloat) has increased by another RMB 400 Million to RMB 1.137 Billion. So it continues to bleed.

So Alibaba is on the hook for both the principal and interest. Tell me again, one more time, why we need Simon Xie involved?

Here's a summary of how Wasu Media has done since the Spring of 2015 when Simon got his hands on the reins of this juggernaut. Looks like the stock tanked from 60 to 8....Ouch! I'll bet that "unnamed Chinese banker" isn't too happy.

Jay Clayton's SEC

Executive Summary:

The SEC, our best and brightest financial regulator is absolutely, completely OK with everything I've described above. Steady as she goes.....don't want to rock the boat. Jay should be really proud of his trained puppy dogs. "Roll over!...Play dead!....that's such a good boy!"

This year: 2018 20-F Pg 61

ITEM 4A. UNRESOLVED STAFF COMMENTS - Not Applicable.

Last yeas: 2017 20-F Pg 115

ITEM 4A. UNRESOLVED STAFF COMMENTS - Not Applicable.

2018 20-F Pg 209

Pending SEC Inquiry